In today’s fast-paced world, quick access to funds can make a significant difference in meeting unexpected expenses or fulfilling personal ambitions. Personal loans serve as one of the most accessible financing options available to consumers in India. However, potential borrowers frequently ask themselves, “What is the actual personal loan approval time in India?” Understanding this timeline can help borrowers prepare adequately. This article will explore the factors that affect personal loan approval time, analyze the differences based on lender type, and highlight the importance of having essential documents like the PAN card ready for smoother processing.

Understanding Personal Loans in India

Before diving into the personal loan approval time based on lender types, it’s essential to grasp what personal loans entail. A personal loan is an unsecured loan provided by financial institutions that borrowers can use for various purposes, such as home renovations, medical emergencies, or travel. Since these loans are unsecured, lenders rely heavily on the borrower’s creditworthiness when making approval decisions.

Factors Affecting Personal Loan Approval Time

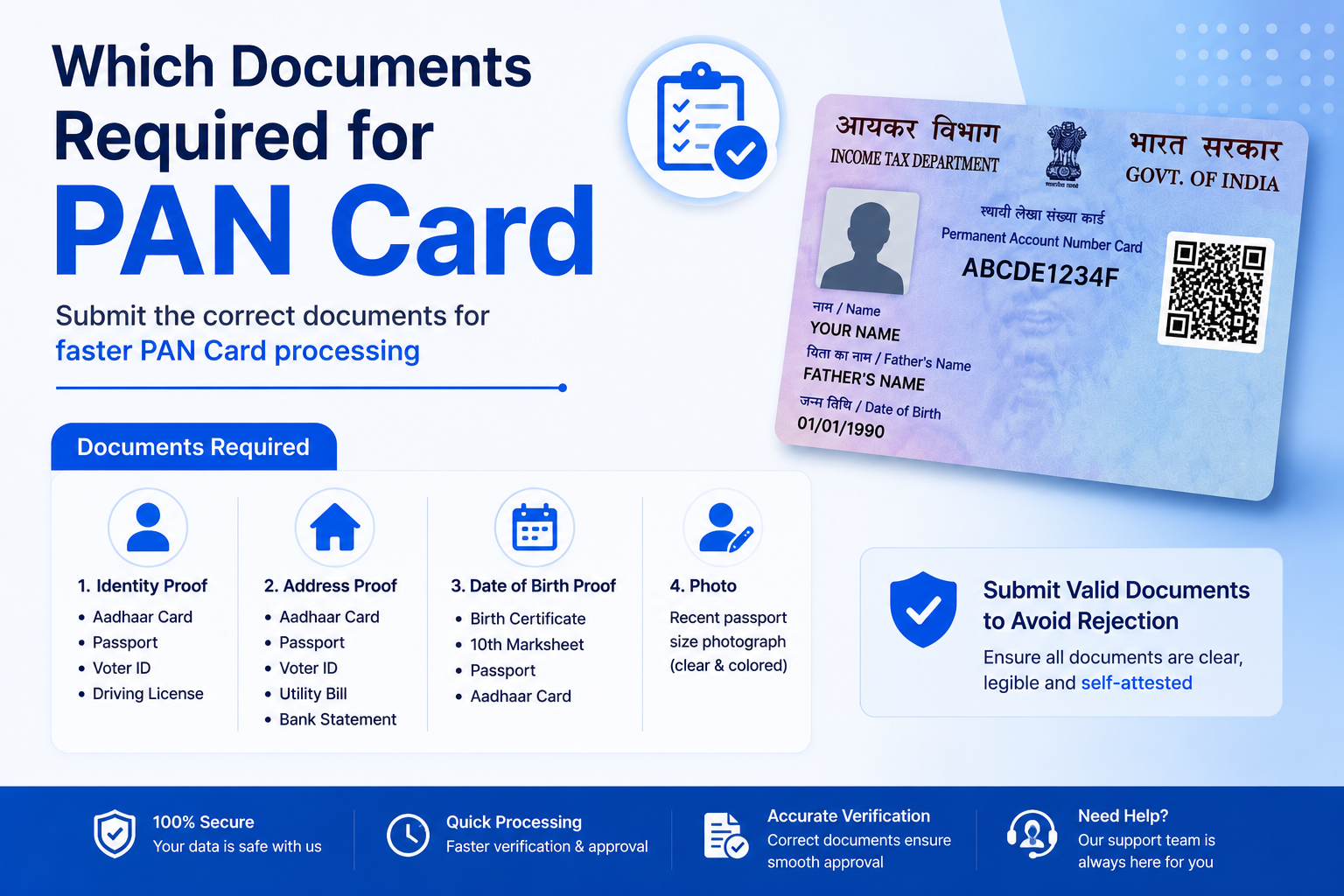

- Documentation: The most critical aspect influencing the time it takes to get a personal loan approved is the documentation. Key documents usually include identification proof, income proof, address proof, and, importantly, the PAN card. Having these documents prepared in advance can significantly reduce approval time.

- Credit Score: Lenders use the credit score to assess a borrower’s creditworthiness. A higher credit score often leads to quicker approvals, while a score below the acceptable threshold can lead to longer waiting periods or outright rejections.

- Income and Employment Stability: A steady income and stable employment history can expedite the approval process. Lenders favor borrowers with regular income streams and job stability.

- Loan Amount and Tenure: The amount applied for and the desired loan tenure also influence approval times. Large loan amounts or extended tenures may require more thorough assessments, thus taking more time.

Lender Types and Their Approval Times

1. Traditional Banks

Traditional banks are commonly considered reliable lenders for personal loans. Their approval process typically involves rigorous checks and balances:

- Approval Time: 7 to 14 days.

- Methods: Lenders verify credit history, employment, and income through thorough documentation.

- Pros and Cons: While traditional banks offer competitive interest rates, the time taken for approval can be longer due to stringent verification processes.

2. Non-Banking Financial Companies (NBFCs)

NBFCs like Bajaj Finance have become increasingly popular in India for personal loans due to their user-friendly approach:

- Approval Time: 3 to 7 days.

- Methods: They often provide a quicker approval process with minimal paperwork, relying more on the applicant’s credit score and fewer physical documents.

- Pros and Cons: While the approval time is significantly faster, NBFCs might charge higher interest rates compared to traditional banks.

3. Fintech Lenders

With the rise of technology, fintech companies have entered the personal loan marketplace, offering innovative solutions.

- Approval Time: Instant to 3 days.

- Methods: These platforms often use online algorithms and machine learning to assess risk more efficiently, allowing for rapid approvals.

- Pros and Cons: While the speed is a significant advantage, borrowers should exercise caution and ensure transparency in the loan terms.

4. Peer-to-Peer (P2P) Lending

P2P lending platforms connect borrowers directly with individual lenders. This model can yield competitive interest rates while offering unique flexibility.

- Approval Time: 5 to 14 days.

- Methods: The approval might involve a less formal process, relying on community-based assessments.

- Pros and Cons: While P2P lending can be faster, factors such as borrower demand and investor willingness can introduce fluctuating times.

The Crucial Role of the PAN Card

Having a Permanent Account Number (PAN) card is crucial when applying for a personal loan. Most lenders require this document as it serves multiple purposes:

- Identity Verification: It helps lenders confirm the identity of the borrower, which is vital for compliance with regulations.

- Financial Assessment: Lenders often use the PAN card to trace a borrower’s credit history and income sources, allowing for an accurate evaluation of creditworthiness.

- Tax Compliance: The PAN card also ties the borrower to their tax obligations. This compliance adds an additional layer of security for the lender.

How to Expedite Approval Using Your PAN Card

- Complete Accuracy: Ensure that all details on your PAN card match your other official documents to avoid discrepancies during the approval process.

- Prioritize Availability: Having your PAN card readily available will save time during the documentation phase.

- Utilize Online Services: Many lenders offer online applications that allow for faster processing times. Make sure to upload accurate and clear documentation, including your PAN card.

Conclusion

The actual personal loan approval time in India varies significantly based on the type of lender you choose. Traditional banks tend to take longer due to their thorough verification processes, while non-banking financial companies and fintech lenders provide more rapid approvals. The essential role of the PAN card cannot be overstated; it not only serves to verify identity but also aids in expediting the overall approval process.

Ultimately, prospective borrowers are encouraged to gather their documentation, especially their PAN card, well in advance and choose the type of lender that suits their speed and financial requirements. By understanding the nuances of the approval process, borrowers can take confident steps toward securing the personal loans they need.

Leave a Reply