When considering any financial decision, especially one involving loans, understanding how to calculate interest rates is crucial. This knowledge empowers you to make informed choices, ensuring that you are not caught off guard by unexpected costs. Let’s delve into the various aspects of calculating interest rates, including its significance and practical application in fields like emergency loans.

What is Interest Rate?

An interest rate is the cost of borrowing money, typically expressed as a percentage of the total loan amount over a specific period. When you take out a loan, lenders charge you interest as a way to compensate for the risk they take by lending you money. For example, if you borrow 1,000 with a 5% interest rate, you’ll owe 1,050 at the end of the repayment period if no other fees or changes occur. Understanding how to calculate interest rate can help you estimate your borrowing costs, compare loan offers, and make more informed financial decisions.

Understanding Types of Interest Rates

There are two primary types of interest rates: fixed and variable.

- Fixed Interest Rate: This is a stable interest rate that remains the same throughout the life of the loan. Borrowing with a fixed rate can be beneficial if you want predictable monthly payments.

- Variable Interest Rate: This rate can fluctuate based on the market conditions or specific financial indices. While it may start lower than a fixed rate, it can increase, leading to higher payments over time.

The Importance of Calculating Interest Rates

Knowing how to calculate your interest rate before signing any agreement is pivotal. Here are several reasons why:

- Budgeting: Understanding interest rates allows you to budget accurately for repayments.

- Comparative Shopping: By calculating rates, you can better compare different loan offers.

- Avoiding Debt Traps: Knowing the right rate helps avoid loans that may lead to overwhelming debt, especially with types like emergency loans.

- Informed Decision-Making: When you understand interest rates, you can confidently negotiate terms or even reject unfavorable offers.

How to Calculate Interest Rate

Calculating the interest rate may seem daunting at first, but with a clear understanding and application of formulas, it can be easy. Below, we will go through the steps involved in calculating your interest rate.

1. The Basic Formula for Interest Calculation

The most basic formula for calculating simple interest is:

[ = P r t ]

Where: – P = Principal amount (initial amount of the loan) – r = Annual interest rate (in decimal form; for example, 5% becomes 0.05) – t = Time period (in years)

Example:

If you borrow 1,000 (P) at an annual percentage rate of 5% (0.05) for 3 years (t), the interest calculated would be:

[ = 1000 = 150 ]

Thus, the total amount owed after 3 years would be 1,150.

2. Understanding APR and APY

When dealing with loans, it’s essential to distinguish between the Annual Percentage Rate (APR) and the Annual Percentage Yield (APY):

- APR: Reflects the annual cost of borrowing on a loan, accounting for interest and fees, but not compounding.

- APY: Takes into account the effects of compounding during a year, offering a more accurate picture of what you’ll earn or owe by the end of the period.

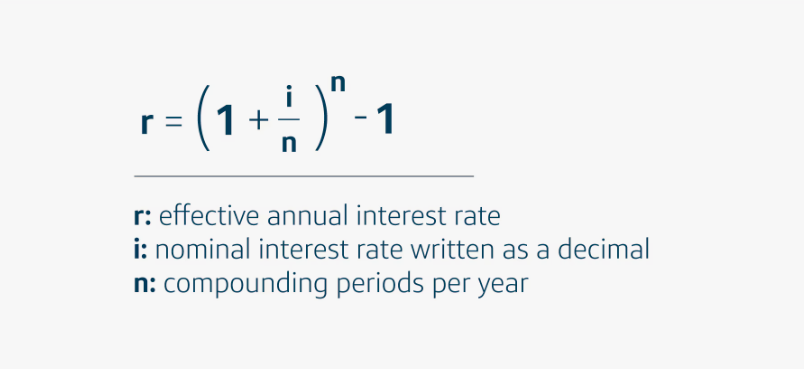

3. Adding Compound Interest

If your loan compounds interest, the formula changes slightly. The compound interest formula is:

[ A = P (1 + )^{nt} ]

Where: – A = the amount of money accumulated after n years, including interest. – n = number of times that interest is compounded per year.

Example:

Using the principal of 1,000, a rate of 5% compounded annually for 3 years, the calculation would be:

[ A = 1000 (1 + )^{1 } = 1000 (1.05)^3 ]

In this case, you would owe approximately 1,157.63 after 3 years.

Special Considerations with Emergency Loans

When applying for emergency loan, it’s essential to understand the interest rates involved. Emergency loans are often quick, short-term financing options that can carry higher interest rates due to their unsecured nature and rapid approval process. Here are some tips for evaluating their costs:

- Read the Fine Print: Always check for hidden fees and conditions tied to the interest rate.

- Understand the Terms: Make sure you comprehend the repayment terms, including any penalties for early repayment.

- Calculate the Total Cost: Calculate not just the interest but the total amount you will have to repay before signing anything.

Conclusion

Before signing any loan agreement, particularly for emergency loans, knowing how to calculate interest rates is an indispensable skill. It helps you understand the true cost of your borrowing, enabling you to budget, compare offers, and make informed decisions. By grasping the differences between simple and compound interest, APR, and APY, you position yourself better to negotiate favorable loan terms. Remember: the better prepared you are, the less likely you are to fall into debt traps. Taking the time to calculate and understand interest rates may be the difference between a successful financial decision and a regrettable one. Always keep this knowledge close to heart as you embark on your borrowing journey.

Leave a Reply